Power market overview Q2 2026

Baltic Prices Rise, but Estonia Stays Cheaper

- Finland and Baltics Converge in April

- Baltic Prices Rise in May and June, Led by Latvia and Lithuania

- Q3 Outlook: Calmer Summer, Rising Risks into September

Finland and Baltics Converge in April

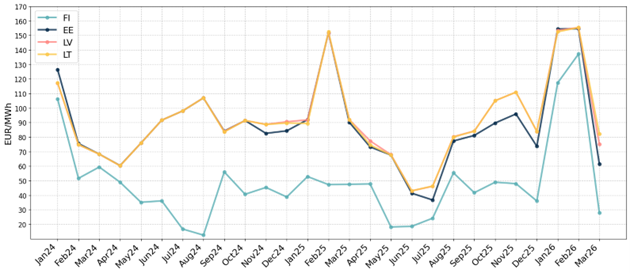

Figure 1 2024-2026 Month average electricity spot prices

After a volatile winter, April was the calmest month of the quarter. Finnish and Baltic prices moved towards each other and settled in a narrow band: Finland averaged 49.5 EUR/MWh, Estonia 54.4, Latvia 57.4 and Lithuania 58.2. Finnish prices rose from a very low March level of 27.8 EUR/MWh, while Baltic prices fell.

Figure 2 Month average solar power generation in Latvia

Several factors pulled Baltic prices lower. Wind conditions were above the long-term average across the Baltics, while Finland saw close to normal wind. Solar generation continued to grow and contributed more than in previous years, with the largest change coming from the solar capacity Latvia has added since last spring. Latvia’s run-of-river hydro also returned to more typical levels after an unusually weak 2025, adding further low-cost local supply. On the Finnish side, some nuclear capacity entered its annual maintenance in April, which trimmed the regional surplus and helped lift Finnish prices back towards Baltic levels.

Baltic Prices Rise in May and June, Led by Latvia and Lithuania

Through May and June, Baltic prices climbed steadily, and the rise was uneven across the region. Latvia and Lithuania led higher, reaching around 82 EUR/MWh in May and 92–94 EUR/MWh in June. Estonia followed more modestly, at 60 and 64 EUR/MWh, while Finland stayed the cheapest area. As a result, the Estonia–Latvia spread widened sharply through the quarter — from only a few EUR/MWh in April to around 22 in May and close to 28 in June. Over the quarter as a whole, Estonia’s average was little changed from a year earlier, while Latvia and Lithuania were up by roughly 15 EUR/MWh.

Figure 3 Nordic Hydro Balance

Two developments lifted the whole region. Baltic wind generation fell, reducing local supply, while the wider market was considerably more expensive than a year earlier. Low Nordic hydro reservoir levels and higher fuel costs — notably TTF gas — pushed the Nordic system price and Continental prices well above 2025 levels. This matters for the Baltics because Lithuania connects directly to southern Sweden through the NordBalt cable, so the SE4 price sets much of the cost of imported power: SE4 averaged around 87–95 EUR/MWh in May and June, against 37–55 a year earlier. Solar remained plentiful and kept midday prices low, but for much of the day the region leaned on this more expensive imported power.

The Estonia–Latvia interconnection explains why the price increase was uneven. Available capacity on the link was reduced, and the TSOs reserve a large share of it for balancing reserves, leaving little room for commercial flows. With power flowing mainly south, the limited Estonia–Latvia capacity was often fully used. Estonia stayed close to low Finnish prices, while Latvia and Lithuania had to cover the shortfall with expensive imports from Sweden. In April the constraint had been far less binding, as strong local generation — including Latvia’s recovered run-of-river output — reduced the need to import through the bottleneck.

Q3 Outlook: Calmer Summer, Rising Risks into September

We expect July and August to be softer months. Demand is seasonally low over the summer, and Finnish nuclear availability should be good, which together point to lower prices. September is more likely to firm up: demand starts to recover as the weather cools, and around 40% of Finland’s nuclear capacity is scheduled for maintenance, including the annual Olkiluoto 3 outage. That would reduce the low-cost Finnish supply the Baltics have leaned on and add upward pressure late in the quarter.

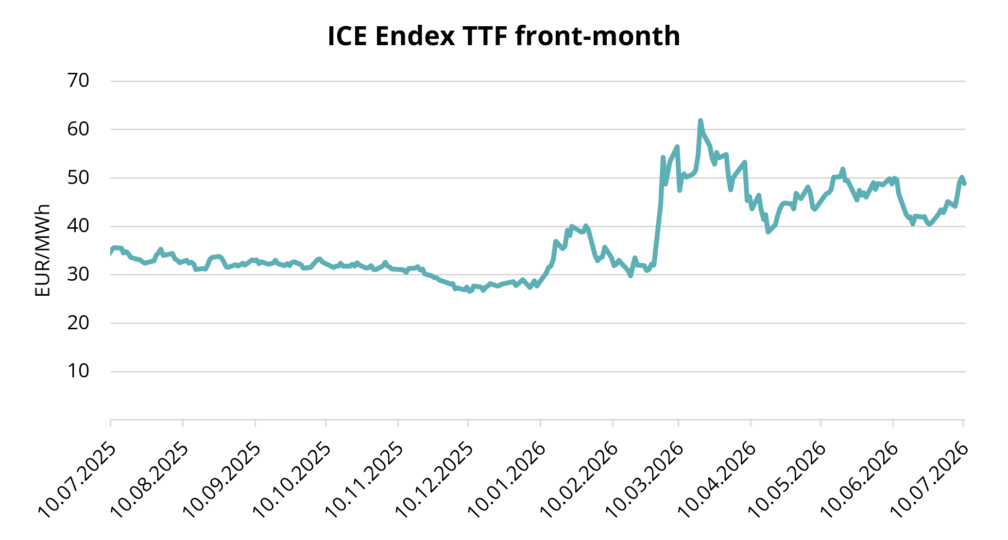

We expect the Estonia–Latvia price difference to persist through Q3. As long as the interconnection stays constrained and flows run mainly southward, Estonia is likely to remain cheaper than Latvia and Lithuania. As always, wind and solar output will be the main swing factor, and an unusually windy or wet Nordic summer could soften the picture. Gas is the other wild card: with tensions around the US–Iran crisis still unresolved, any renewed rise in TTF prices would feed straight through to the Nordic and Continental markets the Baltics import from and push regional prices higher.